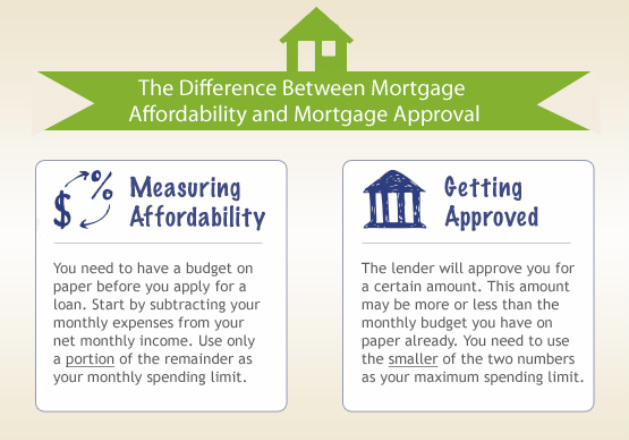

Now That You Know What You Can Afford

Become a Credible Buyer And Get Pre-Approved!

What is Mortgage Pre-approval?

Though there are several different definitions of "pre-approval" used in the mortgage industry, a pre-approval generally is a written statement from a lender stating the lender’s preliminary determination that a borrower would qualify for a particular loan amount under that lender's guidelines. The determination and loan amount are based on income and credit information. Most pre-approval letters are good for 60 to 90 days.

Mortgage pre-approval is a tool you can use to connect with a top lender, who will conduct a preliminary review to determine your loan qualifications based on their guidelines.

Steps are as follows:

Does Pre-approval Guarantee a Loan?

No. Even if you receive a pre-approval letter from a lender, you may not get a loan from a lender and you are not guaranteed a specific rate or loan term.

Regardless of pre-approval, a lender may require additional income and asset verification, as well as the satisfaction of other conditions, before extending you a loan. Pre-approval letters are subject to modification or cancellation if your financial situation or other conditions change.

A pre-approval letter is not an offer to lend, a commitment to make a loan, or a guarantee of specific rates or terms. This online questionnaire is not an application for credit. Also, having a pre-approval letter does not guarantee that an offer you make on a home will be accepted by a seller.

Why Should You Get Pre-approved?

There are many reasons why you should get pre-approved. The most important reason is that you will get an accurate idea of how much home you can afford. This can help to target your home search and ensure you only look at houses that are truly in your price range.

A pre-approval letter also helps you prove to real estate agents and sellers that you’re a credible buyer and able to act fast when you find the home you want to buy. Some sellers might even require buyers to submit a pre-approval letter with their offers, though having a pre-approval letter does not guarantee that your offer will be accepted by a seller.

A pre-approval letter can make you stand out in a competitive real estate market. If you make an offer on a house without a pre-approval, your offer may not be taken as seriously as an offer from another person with a pre-approval.

How Long Does It Take to Get Pre-approved?

Qualified buyers can get a sharable and printable pre-approval letter within minutes. With traditional pre-approval, the process generally takes 24 to 48 hours.

What details are required in the Pre-approval Process? A lender will generally start by asking for some basic information about you and your financial history. If you have a co-borrower, the lender will also need this information about them. Generally, a lender will then request your Social Security number and permission to pull your required credit report (and your co-borrower’s, if you have one). If the information you provide and the information obtained from your credit report satisfies the lender’s guidelines, the lender will make a preliminary determination in writing stating that you would qualify for a particular loan amount subject to the conditions outlined in your pre-approval letter. Please note that each lender has its own standards and processes for determining whether to grant a pre-approval letter.

What If You Can't Get Pre-approved?

If you’re not issued an online pre-approval letter, you can discuss your options with a lender who, with additional information, may still be able to pre-approve you.

Some other things you can do:

Be sure to ask your lender for tips on how you can improve your chances of qualifying for a loan.

Though there are several different definitions of "pre-approval" used in the mortgage industry, a pre-approval generally is a written statement from a lender stating the lender’s preliminary determination that a borrower would qualify for a particular loan amount under that lender's guidelines. The determination and loan amount are based on income and credit information. Most pre-approval letters are good for 60 to 90 days.

Mortgage pre-approval is a tool you can use to connect with a top lender, who will conduct a preliminary review to determine your loan qualifications based on their guidelines.

Steps are as follows:

- Complete a short online questionnaire that asks for information including income, credit score and monthly debt.

- After completing the questionnaire, you will see an estimated pre-approval amount based on the information you provided.

- To continue the process of requesting a pre-approval letter, a lender will require more details, such as pulling your credit report (at your request).

- If you meet the lender’s guidelines based on preliminary review of your responses to the questionnaire and your credit report, you will receive an online pre-approval letter.

Does Pre-approval Guarantee a Loan?

No. Even if you receive a pre-approval letter from a lender, you may not get a loan from a lender and you are not guaranteed a specific rate or loan term.

Regardless of pre-approval, a lender may require additional income and asset verification, as well as the satisfaction of other conditions, before extending you a loan. Pre-approval letters are subject to modification or cancellation if your financial situation or other conditions change.

A pre-approval letter is not an offer to lend, a commitment to make a loan, or a guarantee of specific rates or terms. This online questionnaire is not an application for credit. Also, having a pre-approval letter does not guarantee that an offer you make on a home will be accepted by a seller.

Why Should You Get Pre-approved?

There are many reasons why you should get pre-approved. The most important reason is that you will get an accurate idea of how much home you can afford. This can help to target your home search and ensure you only look at houses that are truly in your price range.

A pre-approval letter also helps you prove to real estate agents and sellers that you’re a credible buyer and able to act fast when you find the home you want to buy. Some sellers might even require buyers to submit a pre-approval letter with their offers, though having a pre-approval letter does not guarantee that your offer will be accepted by a seller.

A pre-approval letter can make you stand out in a competitive real estate market. If you make an offer on a house without a pre-approval, your offer may not be taken as seriously as an offer from another person with a pre-approval.

How Long Does It Take to Get Pre-approved?

Qualified buyers can get a sharable and printable pre-approval letter within minutes. With traditional pre-approval, the process generally takes 24 to 48 hours.

What details are required in the Pre-approval Process? A lender will generally start by asking for some basic information about you and your financial history. If you have a co-borrower, the lender will also need this information about them. Generally, a lender will then request your Social Security number and permission to pull your required credit report (and your co-borrower’s, if you have one). If the information you provide and the information obtained from your credit report satisfies the lender’s guidelines, the lender will make a preliminary determination in writing stating that you would qualify for a particular loan amount subject to the conditions outlined in your pre-approval letter. Please note that each lender has its own standards and processes for determining whether to grant a pre-approval letter.

What If You Can't Get Pre-approved?

If you’re not issued an online pre-approval letter, you can discuss your options with a lender who, with additional information, may still be able to pre-approve you.

Some other things you can do:

- Work to improve your credit score. Your credit score is impacted by payment history, outstanding debt, the length of your credit history, recent new credit inquiries, types of credit used, and more. Generally a score of 720 and higher will get you the most favorable mortgage rates.

- Correct any errors on your credit report, which could help to raise your credit score. The lender will analyze your credit report for any red flags, such as late or missed payments or charged-off debt.

- Decrease your overall debt and improve your debt-to-income ratio. In general, a debt-to-income ratio of 36 percent or less is preferable; 43 percent is the maximum ratio allowed. Use our debt-to-income calculator to determine your debt-to-income ratio.

- Increase your down payment amount in order to qualify for a larger loan. Not able to come up with a down payment? Lean more here!

Be sure to ask your lender for tips on how you can improve your chances of qualifying for a loan.

The Ken Caiani Group with Fairway Independent Mortgage Corporation. Ken Caiani NMLS# 46542 / CO MLO# 100018072 NMLS Consumer Access. FIMC is an Equal Housing Lender and is licensed through NMLS #2289. Regulated by the division of real estate.